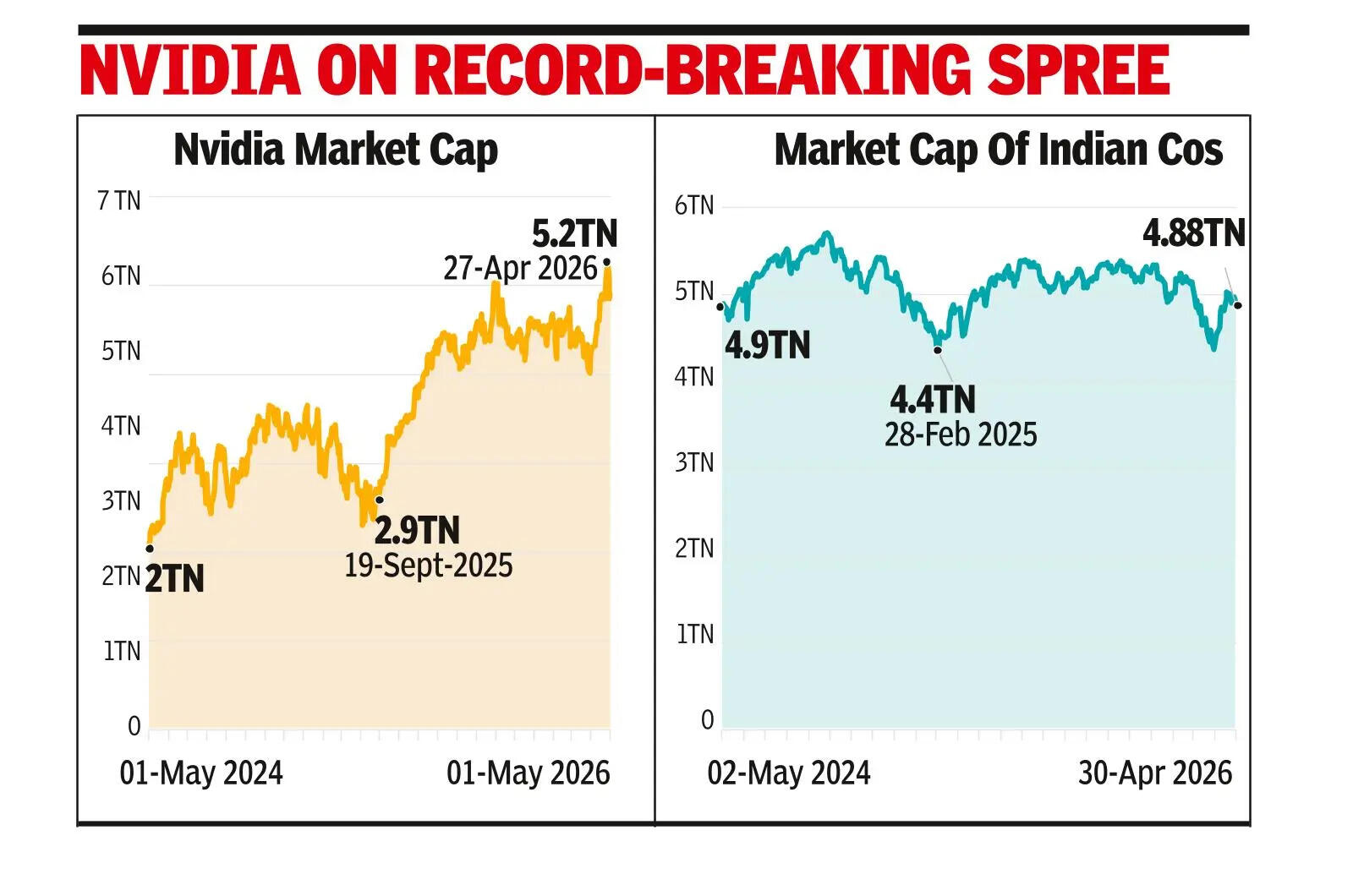

MUMBAI: Nvidia, the global US-based chip giant that’s at the forefront of the ensuing AI revolution across the world, now has a market capitalisation more than the total market cap of all the companies listed in India. Compared to the company’s valuation of $4.91 trillion during opening trades on Friday, India’s was at $4.88 trillion when the local markets closed Thursday, Bloomberg data showed.In the last few years, the demand for AI chips has more than doubled Nvidia’s market cap from about $2 trillion exactly two years ago. In contrast, the slide in the Indian market mainly due to selling by foreign funds and the weakness of the rupee, have left its market cap almost unchanged on a point-to-point basis. In between, it had spiked to an all-time high at $5.9 trillion by end-Sept 2024, around the time the sensex had gone past the 86K mark for the first time in history.

Last week, Nvidia’s market cap had crossed the $5 trillion mark to hit an all-time high at $5.3 trillion. In 2023, it had become the first company in history to hit the $1 trillion market cap and early last year it had become the first to hit the $4 trillion valuation mark.On Oct 29 last year, the chip giant had become the first company in history to hit the $5 trillion market cap mark. Since then, it has had a rough patch on Wall Street and hit a low of $4.2 trillion on March 20 this year. But since then, the revival of the AI rally has revived the Santa Clara, California-based company’s total market value. In the last two years, while Nvidia (and several other tech giants globally) have seen their market values jump substantially, led mainly by the AI-led demand and spending both, the Indian market has been witnessing substantial volatility with a downward bias.According to market players, by Sept 2024, the valuations of the two leading Indian indices—sensex and Nifty—were at multi-year highs (over 25x price-to-earnings or PE for sensex and over 24x for Nifty). Around that time the valuations of several other emerging market countries like India were available at a much lower valuation.During that time, growth of Indian firms was also faltering. The combined effect prompted foreign funds to book profits in the Indian market and invest where valuations were cheaper.