")

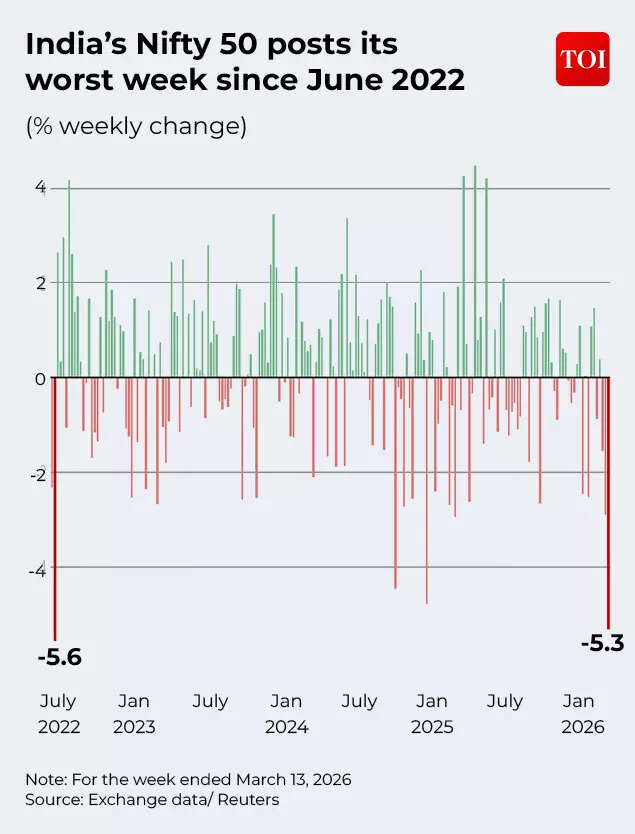

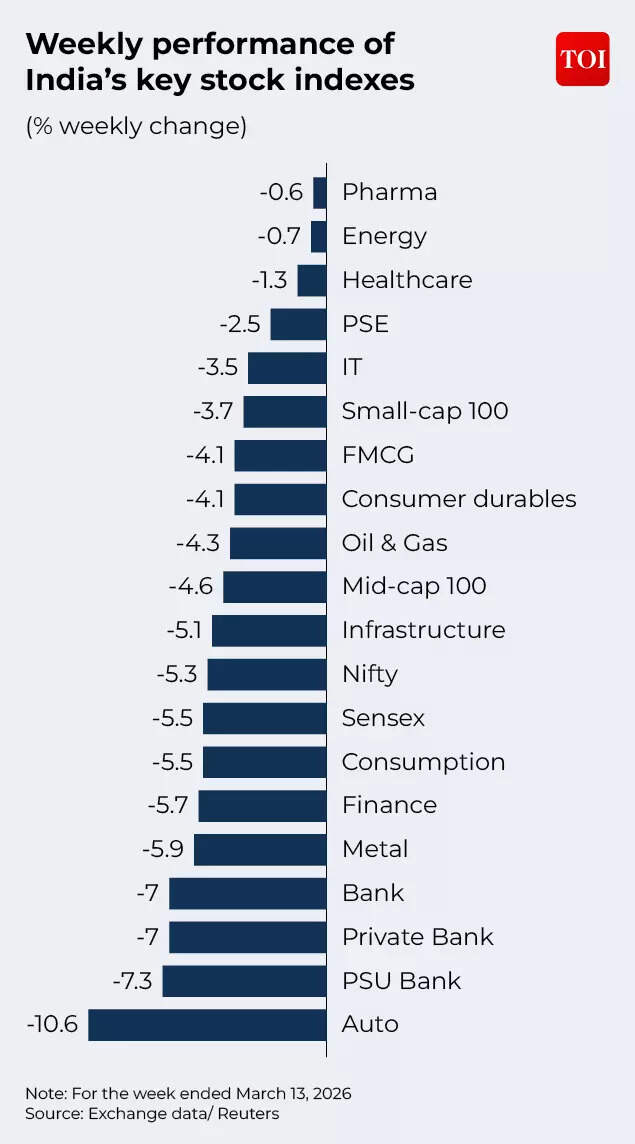

Indian equity markets have witnessed a ‘crude’ shock! The US-Iran war and rising oil prices have spooked investors globally, and Sensex and Nifty are not immune to the selloff. Since the start of the US-Israel-Iran conflict, investors in Indian stock markets have lost several lakh crore and with the war not showing any signs of ending, it is anybody’s guess where and when this bloodbath on Dalal Street will stop.The numbers are staggering: on February 27 the combined market capitalisation of BSE-listed companies was Rs 46,325,200.41 crore. As of March 13, 2025, it has fallen to Rs 42,939,960.29 crore. That’s a loss of almost Rs 34 lakh crore in investor wealth over a span of two weeks and nine trading sessions! Rising crude oil prices (at one point they almost hit $120!), relentless selling in global markets, continued foreign fund outflows and weakness in the Indian rupee have all weighed on market sentiment. Nifty50 has actually seen its biggest weekly drop in years.The closure of Strait of Hormuz is hitting not just oil and LPG supply, but also other trade, which may ultimately hit across sectors in India. So what does this mean for investors – should they stay invested in equities?

Stock market check: Is the long-term growth story intact?

Market experts caution that in times of geopolitical tensions, even routine corrections can appear far more worrying than they really are. They believe that from the standpoint of Indian investors, the longer-term outlook for the Indian equity market remains constructive. They also point to India’s strong growth trajectory amidst global crises.

According to Moody’s Analytics, rolling 12‑month drawdowns from recent peaks show that China and India have experienced relatively modest pullbacks, broadly in line with their usual market swings. “Although both economies are large net oil importers from Gulf Cooperation Council economies in absolute terms, energy imports account for a smaller share of domestic consumption, limiting their vulnerability to oil price shocks. Foreign investor participation in equity markets is also lower, and in China’s case, capital controls further limit volatility. These structural factors have helped shield their equity markets from sharper declines,” it says.Vinod Nair, Head of Research at Geojit Investments Limited is confident that India’s long-term growth and investment story remains intact. “Structural drivers such as rising domestic consumption, sustained infrastructure investment, widespread digital transformation, and improving corporate balance sheets continue to support the broader market outlook. This is further reinforced by policy support for manufacturing, the energy transition, tax reforms, infrastructure development, and a pickup in private capital expenditure,” Nair tells TOI.A key thesis is that the current US–Iran war is likely to be short-lived. While it has led to a contraction in valuations below long-term averages, this is expected to trigger a sharp rebound in the coming months, driven by deep value buying. Importantly, the earnings outlook for FY27 remains strong, with high mid-teen growth still intact, he adds.

Sunny Agrawal, Head – Fundamental Research at SBI Securities points to historical data to note that the market always climbs the wall of worry. “Markets have historically witnessed many wars, domestic and global macro economic challenges, life threatening waves of disease and every time have managed to scale new highs. Moreover, historical data suggests that after a period of no returns for 17 months, equities have delivered fabulous returns over the next 6 months to 3 years,” he tells TOI.Experts are also of the view that with the stock market seeing sharp corrections over the last few months, valuations are attractive.Vijay Kuppa, CEO of InCred Money explains that Indian stock markets have been impacted because of the severe outflow of FIIs which was mainly due to the elevated valuations and also because India is not considered a big part of the AI theme.“From a macro-standpoint, India is positioned well. This can be disrupted if the Iran conflict continues and oil prices remain elevated for a longer time. The present sense is that prices will come down sooner than later. Investor enthusiasm seems to be fatigued with flat markets over the last 18 months or so. But with valuations compressing and with FII holdings already at multi-period low, this underperformance may not continue for long,” he tells TOI.Chirag Muni, Executive Director at Anand Rathi Wealth Limited explains the fundamentals in detail: If we look at the next 5 years, we see that India’s economic fundamentals continue to provide a strong base. Real GDP growth is expected to stay in the 6–7% range, and inflation is likely to remain around 4–5%. Hence, nominal GDP growth around 11–12% can be expected. Thus, over the long term, this supports corporate earnings and equity markets, he tells TOI. He goes on to elaborate: It is important to understand the current market volatility in context of market behaviour in the long term. “Since 2001, we see that a drawdown of around 18% is normal and markets have usually taken just a year to recover from such phases. Even during periods of geopolitical uncertainty as we are seeing right now, Nifty has seen corrections of around 5–7%, and in most cases has bounced back within about a month. Thus, the current fall does not appear to be concerning,” Muni says.According to Muni, domestic participation is also an important stabilising force. In 2025, domestic institutional investors invested about ₹7.88 lakh crore into equity even as foreign investors sold roughly ₹1.66 lakh crore. In March 2026, small cap funds still saw around ₹700 crore of net inflows. “This shows that investors are not reacting out of fear and continue to maintain balanced allocations across market caps,” he says.

What should investors do?

So, if experts are of the view that the long-term equity market story is still in place, what should investors do in the current scenario?The SBI Securities expert is of the view that the ongoing Middle East war and its pursuant impact on the global energy prices is likely to recede in the next few weeks. “Investors should use this opportunity to deploy long term capital in equities in quality, fundamentally sound businesses across large, mid and small caps. Sectors which are likely to outperform are BFSI, Auto/Auto Ancillary, Consumer Discretionary, New Age Businesses, Power/Power Ancillary etc.,” he says.Vijay Kuppa of InCred Money points out that there has been a decent price and time correction in the small and midcap space where valuations have corrected materially in some spaces as investors chase earnings growth over plain narratives. “Investors should start deploying a percentage of their opportunity fund at every dip. If investors are not comfortable taking direct positions in stocks, they can look at ETFs or Mutual Funds to take exposure,” he says.Experts pitch for staying the course and maintaining a balanced portfolio allocation.Chirag Muni of Anand Rathi Wealth recommends that long-term investors should remain disciplined, stay on course for their investment strategy and avoid reacting to headlines. “They should stay consistent with the long-term asset allocation that was originally planned, with a balanced allocation of around 80% in equity and 20% in debt. Within the equity portion, they should stay invested in diversified equity mutual funds, with a 55% allocation to large caps, which helps provide stability, and the rest in mid and small caps, allowing them to benefit from the high growth potential of the same,” he tells TOI. Market corrections of around 10–15% can even be seen as opportunities to deploy additional capital into the market, allowing investors to benefit from the eventual recovery that will follow and build long-term wealth, he adds.While experts express confidence in the long-term growth story, Thomas V Abraham, Research Analyst at Mirae Asset ShareKhan strikes a more cautious note.“Prolonged disruptions amplify vulnerabilities, eroding corporate margins, deferring capex, and curtailing EPS growth in energy-exposed sectors like manufacturing, pharma, and hospitality. Nifty EPS growth could moderate in FY27, with cyclicals (oil & gas, autos) facing outsized pressure; upstream OMCs may see near-term gains from realizations,” he tells TOI.The expert says that with valuations compressed, investors should maintain existing positions but rebalance for resilience. “Deploy fresh capital opportunistically, staggering entries into fundamentally robust names. Expect revival over 6-8 quarters as green shoots emerge, supporting valuation recovery,” he says.Thomas V Abraham’s recommended allocation is:

- Defensives (60-70%): Pharma (domestic formulations for volume resilience; export-led for forex hedges) and FMCG (staples with pricing leverage).

- Opportunistic (20-30%): Provides a good opportunity to accumulate large cap companies such as RIL at a lower valuation.

- Hedges (10%): Gold / Gold ETFs/sovereign bonds; 3-6 month FDs yielding 7-8% for liquidity.

This mix leverages the benefit of pharmaceuticals and other sectors during this volatile period while also prioritizing stability, he concludes.(Disclaimer: Recommendations and views on the stock market, other asset classes or personal finance management tips given by experts are their own. These opinions do not represent the views of The Times of India)