")

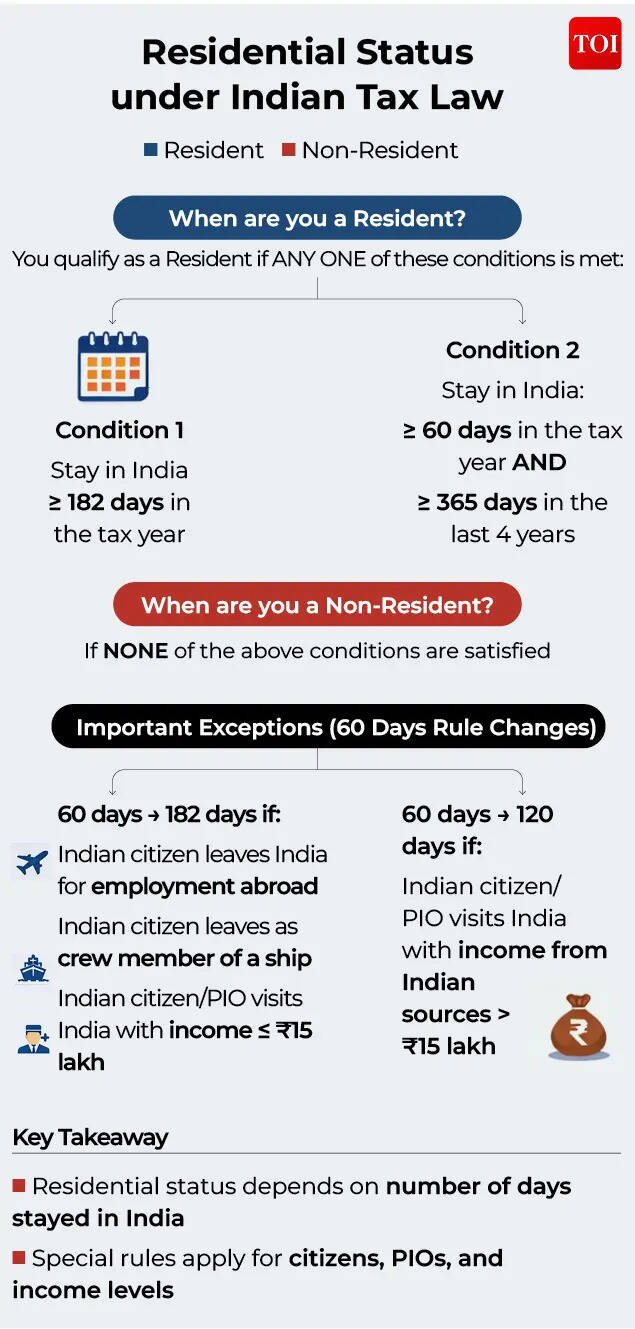

In today’s globalised world, the ability to live in one country and work in another country for an employer in the third country is becoming a norm rather than an exception. Professionals are increasingly building careers across borders as organisations are increasingly hiring best talent to support them from anywhere. Amid this growing talent fungibility, the factors that play a vital role in determining tax liability depending on one’s country are residential status, citizenship, situs of income, etc.. However, determining residential status varies from country to country and it could be complex due to various possible interpretations.As per Indian tax laws, the extent to which an individual shall be taxed is determined based on their residential status. We have attempted to bring out a comprehensive understanding of India’s residency rules, read in conjunction with international tax principles and treaty frameworks for accurately determining tax exposure in a cross-border context.How India’s residency rules differ from other countriesIndia determines an individual’s tax residency primarily on the basis of physical presence (irrespective of the purpose of stay) within the country. The number of days present provides a mechanical framework for classifying taxpayers’ residential status under Indian tax laws.In contrast, many developed tax jurisdictions adopt a more holistic approach in determining residency. While the number of days present thresholds continue to play an important role globally, countries such as the US, UK, Australia, France etc. supplement physical presence tests with a broader evaluation of an individual’s personal and economic connections. These may include factors such as the location of family, availability of a permanent home, place of employment, domicile, and the centre of economic or vital interests. In certain jurisdictions, additional considerations, such as citizenship, also influence the determination of tax residency.As a result, unlike India’s predominantly physical presence-based framework, several jurisdictions adopt a multi-factor analysis that balances physical presence with qualitative factors reflecting the individual’s broader personal and economic integration within the country. This approach is intended to ensure that tax residency aligns more closely with the individual’s real connection to the jurisdiction rather than being determined solely by thresholds of physical stay.At the international level, the Organisation for Economic Co-operation and Development (OECD) provides guiding principles on tax residency through the OECD Model Tax Convention, which serves as the foundation for many bilateral tax treaties. The OECD framework is particularly relevant in situation of dual residency in order to allocate residency to a single jurisdiction in a manner that reflects the individual’s closest and most substantive connections by way of tie-breaker rules based on criteria such as the existence of a permanent home, the centre of vital interests, habitual abode, and nationality.How to determine residential status as per Indian tax lawsThe Residential status of an individual can be classified into two main categories:An individual would qualify as a Resident if either (1 or 2) of the following two basic conditions are satisfied. If none (1 and 2) of the conditions are satisfied, then an individual would be treated as Non-resident in India:

- He/ she stays in India for 182 days or more during the relevant tax year; (or)

- He/ she stays in India for 60* days or more during the relevant tax year and 365 days or more in four tax years immediately preceding the relevant tax year.

*60 days mentioned in point 2 above should be read as 182 days, if –

- An Indian citizen leaves India for the purpose of employment outside India in the tax year;

- An Indian citizen leaves India as a member of the crew of an Indian ship / foreign bound ship in the tax year;

- An Indian citizen or a person of Indian origin comes on a visit to India in the tax year and have total income from Indian sources up to Rs 1,500,000 during the relevant tax year.

*60 days mentioned in point 2 above should be read as 120 days, if –

- An Indian citizen or a person of Indian origin comes on a visit to India in the tax year having total income from Indian sources exceeding Rs 1,500,000 during the relevant tax year.

Residents in India could be further classified as ‘Resident and Ordinarily Resident’ (ROR) or ‘Resident but Not Ordinarily Resident’ (RNOR).

An individual shall be classified as ROR if both the following conditions are satisfied and as RNOR if either 1 or none of the following conditions are satisfied:

- He/ she qualifies as a Resident (as per basic conditions) in India in two out of ten tax years immediately preceding the relevant tax year; and

- He/ she stays in India for 730 days or more in seven tax years immediately preceding the relevant tax year.

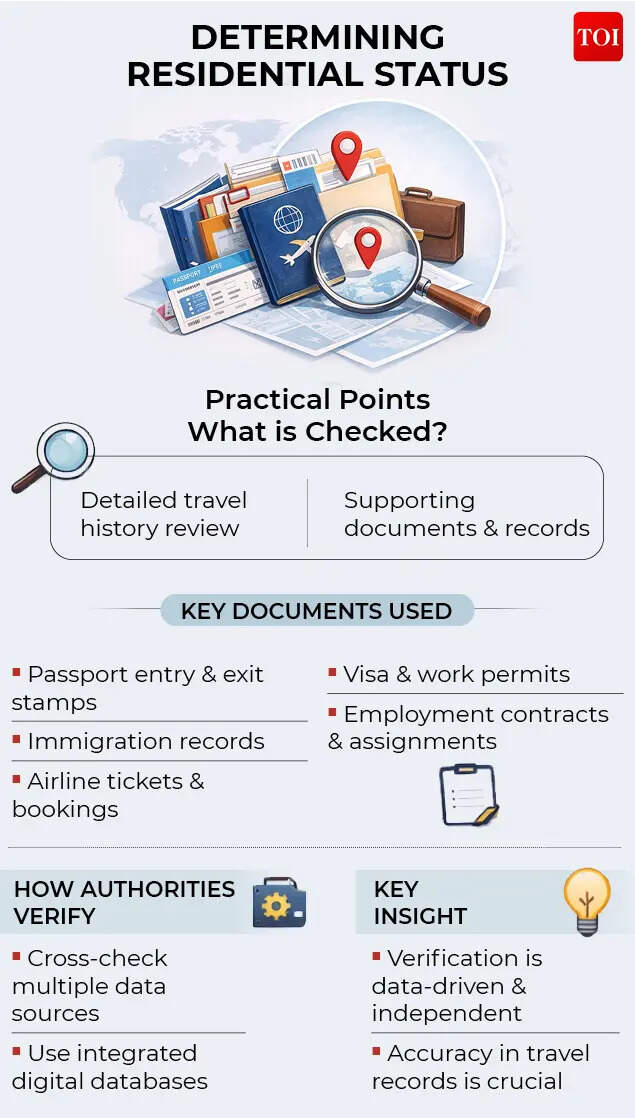

Residential status must be determined separately for each tax year, based on an individual’s physical presence in India during the relevant tax year. In computing the number of days in India, both the day of arrival and the day of departure shall be counted as day present in India.Tax exposure based on residential classificationAn individual qualifying as a ROR is subject to tax in India on their worldwide income and non-resident is subject to tax in India on their Indian source and received income in India. In contrast, a RNOR is liable to tax only on income that is earned or received in India, or income arising from a business controlled or a profession set up in India, with most foreign income remaining outside the Indian tax net.The RNOR classification often serves as a transitional benefit, particularly for individuals returning to India after an extended period of employment overseas, as well as for foreign nationals in the initial years of their stay in India, before their worldwide income becomes fully taxable in India.Illustrative case studiesBelow are some practical illustrations to comprehend how residency rules operate in India.Case Study 1: Leaving India to take up an employment abroadX, an Indian citizen employed with ABC Pvt. Ltd., departs from India on 15 July 2025 to take up an employment assignment in the UK, with the payroll transitioning to ABC Plc UK. During the relevant tax year 2025–26, X was present in India from 1 April 2025 to 15 July 2025 and does not return to India for the remainder of the year ending 31 March 2026.Given that X left India for the purpose of employment outside India, the threshold of 182 days applies for determining his residential status. As his total period of stay in India during the tax year is less than 182 days, X would qualify as a Non-Resident for the tax year 2025–26.Case Study 2: Leaving India for a short-term assignment and returning back to India in the same tax yearConsider a scenario where Y departs from India on 1 June 2025 to take up a short-term assignment in Singapore but subsequently returns to India on 14 December 2025. During the relevant tax year 2025–26, Y is present in India for 62 days prior to departure (1 April to 01 June 2025) and for a further 108 days following return (14 December 2025 to 31 March 2026). Accordingly, the total period of stay in India during the year amounts to 170 days.Given that Y initially left India for the purpose of employment outside India, the 182-day threshold would apply for determining residential status. As the total stay in India during the tax year does not exceed 182 days, Y would qualify as a Non-Resident for tax year 2025-26.Case Study 3: Leaving India for a long-term assignment abroad and returning after few yearsConsider an individual, Z who relocated to the US on 10 August 2023 for employment (never been abroad in the past) and continues to reside in the US for the subsequent years. Z returns to India for good on 20 January 2026 with the intention of residing permanently.During the relevant tax year 2025–26, Z is present in India for 71 days (from 20 January 2026 to 31 March 2026). Prior to departing India in August 2023, the individual had spent a substantial period in India, resulting in an aggregate presence exceeding 365 days during the four tax years preceding tax year 2025–26.In such a scenario, although the individual’s stay in India during the relevant tax year 2025-26 does not exceed 182 days, the individual would nevertheless qualify as a Resident in India by virtue of satisfying the 60 days plus 365 days condition.Practical considerations in determining residential statusIn practice, the determination of residential status necessitates a detailed review of an individual’s travel history and supporting documentation. The Indian tax authorities during assessments rely on multiple data points to verify the period of stay in India, including:

- Passport entry and exit stamps

- Immigration records maintained by authorities

- Airline travel itineraries and booking history

- Visa and work permit documentation

- Employment agreements and assignment letters etc.

With the growing digitisation and integration of immigration and travel databases, tax authorities may verify such information independently.

Some important watch pointsGlobally mobile workforce must have a clear understanding of tax residency rules due to their international travel patterns and overseas assignments.Individuals can avoid the risk of non-compliance by closely monitoring the number of days spent in India during each tax year to reassess their residential status on an annual basis. As the residential status may vary depending on travel patterns and personal circumstances. Particular attention may be paid to specific provisions applicable to Indian citizens leaving India for employment abroad or visiting India and those returning after long overseas assignments.Individuals should effectively apply tie breaker rules in case of possible dual residency under applicable tax treaty provisions.Since India’s residency framework is based on physical days’ presence, therefore adopting a proactive approach by maintaining accurate travel records, understanding the applicable legal provisions, and periodically reviewing one’s residential position may help ensure compliance and avoid any unforeseen tax consequences.(Ravi Jain is Tax Partner at Vialto Partners. Vikas Narang, Director and Pawan Digga, Manager at Vialto Partners have also contributed to the article. Views are personal)